Sydney has always been Australia’s benchmark property market being aspirational, expensive, and built on fundamentals that don’t shift easily. As we move through 2026, it’s doing what Sydney does: holding firm while the louder markets grab the headlines. Brisbane is booming, Perth is surging, Adelaide is turning heads. But dismissing Sydney because other cities are growing faster right now would be a mistake. This is still a city of 5.3 million people, with a permanently constrained land base, one of the tightest rental markets in the country, and a pipeline of infrastructure investment reshaping how and where people want to live.

Here’s what investors actually need to know.

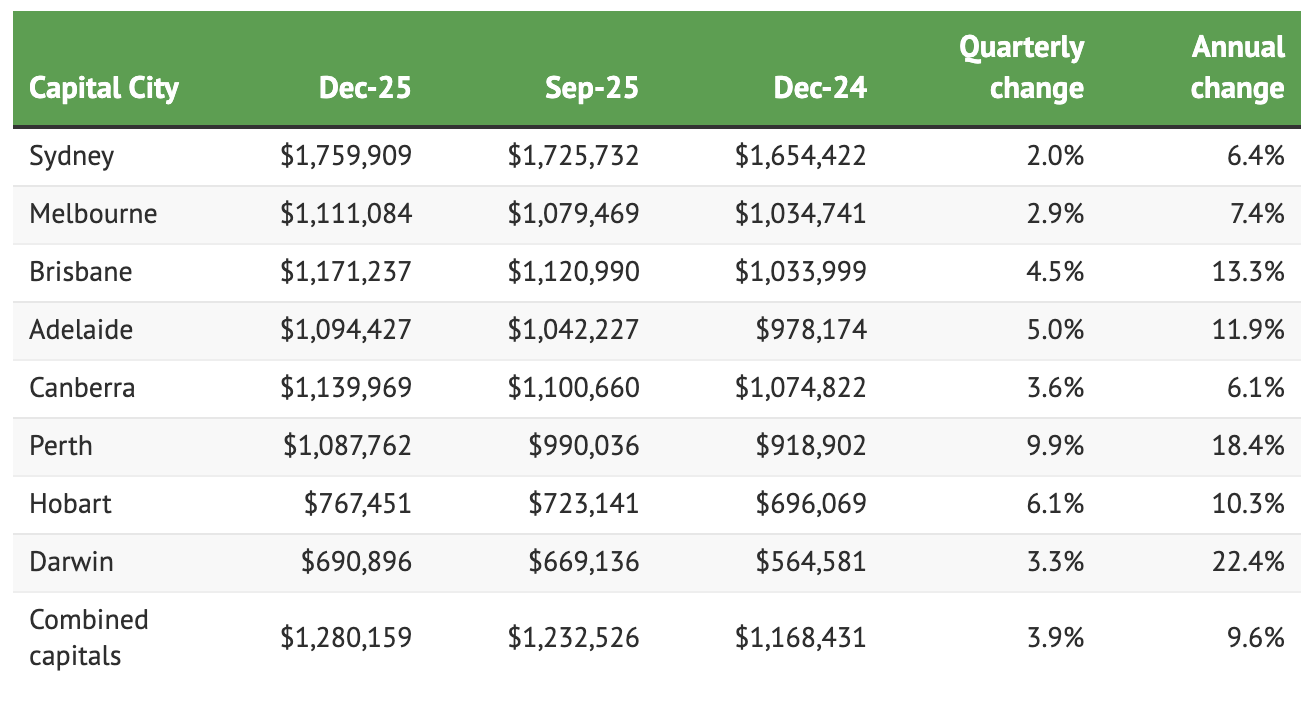

Where Has the Sydney Market Been Over the Last 12 Months?

Sydney grew around 30% through the pandemic years, while other cities were recording gains closer to 70%. The more measured pace we’re seeing now is partly a reflection of that earlier performance and partly a function of affordability constraints that are unique to this city. When property prices are significantly higher than in other capitals, but income levels aren’t dramatically different, buyers naturally start weighing their options more carefully.

What’s worth noting is that Sydney isn’t standing still. The ‘Alice Uribe’ from January 2026, puts annual dwelling growth at 6.4%, and ‘Which Real Estate Agent’ puts with last five-year gains of 31.1%. Houses have outperformed units over the past year, 7.6% versus 3.3%, which reflects a simple reality: detached homes in Sydney are genuinely scarce, and scarcity pushes prices up.

What's Driving and Constraining the Sydney Market in 2026?

Affordability pressure, a constrained land base, and major transport infrastructure are the three biggest forces shaping Sydney’s property market in 2026.

The Affordability Reality

There’s no sugarcoating this: Sydney is the most expensive capital city in Australia by a meaningful margin. Income levels between Sydney, Melbourne, and Brisbane aren’t different enough to explain the price gap, and that’s been redirecting investors and owner-occupiers, toward other markets for several years now.

What affordability pressure does is slow transaction volumes and temper growth at the top end. What it doesn’t do is undermine Sydney’s long-term investment case. The city’s employment depth, migration pull, and constrained housing pipeline provide a floor under values that other markets simply don’t have.

Before buying in Sydney, ask yourself:

- Is my budget realistic for the suburb I'm targeting, or am I stretching into a price point where yield won't work?

- Am I comparing Sydney to Brisbane or Perth on short-term growth or on the long-term capital base I'm buying into?

- Have I accounted for the fact that Sydney's entry price means a larger deposit sitting idle for longer?

Transport infrastructure is genuinely moving prices in parts of Sydney. A commute that once took 50 minutes shrinking to under 20 is the kind of lifestyle shift that changes the numbers buyers are prepared to pay, and well-connected suburbs have consistently attracted stronger buyer demand and faster selling conditions as a result.

Five Dock is a good example of how this plays out in practice. The suburb’s upcoming Metro West station has been woven into virtually every property listing in the area since the moment it was announced, and the market has responded accordingly. According to CoreLogic data, Five Dock has delivered 47.4% growth over the past five years, with much of that momentum building from the point the metro line entered public conversation. The growth story there is real, but it’s worth asking: how much of that upside has already been captured by the people who moved early?

That’s the central tension with infrastructure-driven buying. Cotality’s research on Sydney Metro corridors found that once stations open, surrounding suburbs don’t automatically keep outperforming. In many cases they underperform the broader Sydney benchmark, because the premium was priced in during the announcement and construction phase, not after opening day.

The same zoning changes that enable new metro corridors also open those areas to high-density residential development. Cotality research data from Liverpool makes the point clearly: houses recorded 14.3% annual growth, while units in the same suburb gained just 3.0% over the same period. Parramatta tells a similar story over the longer run. Early buyers near newly announced stations often capture genuine upside. Late buyers into an oversupplied high-rise corridor often don’t.

What Should Property Investors Focus on in Sydney for 2026?

In Sydney’s current market, the strongest opportunities sit in compact, well-located apartments within owner-occupier dominated buildings, where yield is more workable and long-term capital growth is better protected.

Smaller Properties, Better Yield Numbers.

Sydney’s gross rental yields sit around 3.1% across all dwellings, among the lowest of any capital city, and a direct function of its high entry prices rather than weak rents. For investors who need the income side of the equation to work, the unit market is where the better numbers live.

Sydney’s vacancy rate is sitting at approximately 1.3% according to SQM Research well below the 2 to 3% considered a balanced market, and rents have been rising steadily. CBRE’s research projects apartment rents across Australian capitals to grow 24% between 2025 and 2030, with Sydney’s vacancy expected to tighten further as apartment delivery averages just 11,700 per year against annual demand for 30,000 dwellings. That structural undersupply isn’t going away quickly.

One-bedroom apartments and studios in high-demand pockets, the eastern suburbs being the obvious example as it’s commandingly strong weekly rents that can make the yield arithmetic work, even at elevated purchase prices. The psychological hurdle of spending close to a million dollars on a compact property is real. For off-the-plan purchases especially, that capital sitting idle between exchange and settlement, often 12 to 24 months, adds another layer to the decision. ENAYBL’s deposit bond solutions let investors secure their position at exchange without tying up that cash, which in a market this tight, is worth knowing about.

Owner-Occupied Dominated Buildings:

Here’s something the headline data doesn’t capture: the composition of an apartment building is one of the most important factors in its long-term performance, and most buyers never ask the question.

Buildings where owner-occupiers make up the majority of residents hold value better, present better, and attract stronger buyer competition at resale. The people living there have a direct financial interest in the quality of the complex, and that shows up in maintenance standards, strata management, and presentation over time. When it comes time to sell, that difference is tangible.

Investor-heavy buildings face the opposite dynamic. Multiple vendors can hit the market simultaneously. Strata levies can blow out. Presentation slides. And when the next wave of comparable new stock lands nearby, competition for buyers intensifies further. Vacancy is tight across Sydney right now, so finding tenants isn’t the challenge regardless of where you buy. The real differentiator is what happens to your asset’s value over a 10 to 15-year hold, and that’s where building composition pays real dividends.

The High-Rise Near Metro Trap

The pitch sounds reasonable: buy near a new station, ride the connectivity premium, watch values climb. And in the short window around a station announcement, that often plays out. The problem is what comes next.

Zoning changes enabling metro development also green-light significant high-density construction in those corridors. More supply means more competing listings, more investor owners who bought off-the-plan and enter the rental or resale market in the same cycle. The Liverpool and Parramatta apartment data isn’t an anomaly, it’s the predictable outcome of infrastructure-adjacent buying without accounting for what else gets built there.

For investors with a genuine long-term focus, established apartments in suburbs where new supply is genuinely limited, (particularly owner-occupier-heavy complexes away from high-density rezoning precincts) have a far more reliable track record in Sydney than new high-rise product near transport hubs.

Sydney Suburbs to Watch in 2026

Sydney is not one market, it’s dozens of smaller markets defined by price point, proximity to the CBD, infrastructure access, and buyer demographic. The following suburbs represent a cross-section of genuine investment opportunities heading into 2026.

Five Dock – Metro Uplift Already in Motion Median house: $2.79M | Median unit: $1.15M | Unit yield: 3.6%

Five Dock sits 10 kilometres west of the CBD in Sydney’s tightly held inner west, and it has been one of the market’s quiet achievers, 47.4% growth over five years, with the upcoming Metro West station woven into virtually every listing in the area since the announcement was made. The suburb appeals to a high-income, professionally employed demographic, with median household income well above the Sydney average, strong owner-occupier dominance, and very low stock on market.

At a typical house price above $2.7 million, Five Dock is not an entry-level play but for investors focused on long-term capital preservation in a genuinely constrained, high-demand suburb, the fundamentals are hard to argue with. The more important question, as discussed earlier, is how much of the metro uplift has already been priced in. Five Dock is a suburb to watch rather than one where the easy gains still lie ahead. Timing and product selection matter here more than almost anywhere. And when you do move on a property at this price point, a 10% deposit means $270,000 or more sitting idle between exchange and settlement, a deposit bond through ENAYBL can keep that capital working until settlement day.

St Marys – Best Entry Point with a Western Sydney Catalyst Median house: $1.1M | Median unit: $710,000 | Unit yield: 4.3%

One of the few remaining Sydney suburbs where a house median sits at $1.1 million and a unit can be secured around $710,000, and it comes with a genuine, near-term growth catalyst. The Western Sydney Airport at Badgerys Creek is due to open in 2026, and St Marys sits within its employment and connectivity catchment. House prices have already risen 14.9% over the past 12 months, with properties selling in an average of just 17 days, the fastest days-on-market of any suburb in this list. Unit yields are sitting at 4.3%, one of the better income propositions available within Greater Sydney. The buyer profile here is shifting, with owner-occupiers increasingly competing with investors for available stock, historically a signal of a market maturing toward longer hold periods and stronger community investment. For investors seeking an accessible Sydney entry point backed by infrastructure tailwinds that haven’t yet fully played out, St Marys warrants serious attention.

Marrickville – Best Inner West Fundamentals Median house: $2.2M | Median unit: $893,500 | Unit yield: 3.9%

Seven kilometres from the CBD and still delivering. Marrickville has recorded 4.6% annual house price growth and 8.5% across the broader Marrickville-Sydenham-Petersham corridor, making it one of the stronger performing inner-city precincts in Sydney right now. The suburb has undergone a decade of genuine gentrification, with a thriving café culture, new library, and community infrastructure that continues to attract young professionals and families in equal measure.

What makes Marrickville compelling for investors specifically is the unit market, having a median entry point of around $893,500 with yields sitting at 3.9% is as close to workable as Sydney’s inner ring gets. The Sydney Metro City Line extension running through the suburb adds a connectivity layer that will continue to support both rental demand and resale appeal for years ahead. Units here sell in an average of 30 days, a sign of the depth of buyer interest at this price point.

Baulkham Hills – The Underrated North-West Performer Median house: $1.96M | Median unit: $920,000 | Unit yield: 3.8%

Baulkham Hills doesn’t generate the headlines of inner-city suburbs, and that’s precisely what makes it worth a closer look. Located in Sydney’s Hills district, 30 kilometres north-west of the CBD, it offers generous block sizes, elite school zones, and an owner-occupier dominance rate sitting above 77%, one of the highest in Greater Sydney. The unit market has recorded 5.75% annual growth, outpacing the house market in the same suburb and reflecting the broader Sydney trend of units catching up as affordability forces more buyers into medium-density stock. Median unit rents sit at $680 per week with yields of 3.8%, and units are selling in an average of just 25 days. Development approvals in the area are moderate, limiting the oversupply risk that plagues other north-west corridors. For investors who prioritise long-term capital stability in an owner-occupier dominated, supply-constrained suburb without paying inner-city prices, Baulkham Hills consistently delivers.

Suburb | Median House Price | Median Unit Price | Unit Yield | Annual House Growth |

Marrickville | $2,200,000 | $893,500 | 3.9% | 4.6% |

Five Dock | $2,790,000 | $1,150,000 | 3.6% | 2.1% |

St Marys | $1,100,000 | $710,000 | 4.3% | 14.9% |

Baulkham Hills | $1,960,000 | $920,000 | 3.8% | 2.3% |

Source: realestate.com.au / CoreLogic data to November–December 2025

Is Sydney Still Worth Investing In For 2026?

Sydney remains one of Australia’s most reliable long-term property markets, provided investors are selective about location and property type.

Sydney’s long-term case rests on foundations that haven’t shifted: genuine population demand, a land base that cannot materially expand, and a status as Australia’s economic capital that no other city is close to displacing. Limited new supply, elevated construction costs, and cautious dwelling delivery are all expected to keep a floor under prices through 2026 and beyond.

The investors who struggle in Sydney tend to buy the wrong product in the wrong location, new high-rise in an oversupply corridor, or an investor-heavy complex where the next wave of comparable stock is already under construction nearby.

Sydney rewards patience and selectivity.

The investors who do well ask better questions before they sign anything:

- Does this building have a strong owner-occupier presence?

- Is this suburb genuinely supply-constrained, or is it earmarked for densification?

- Has the nearby infrastructure already been fully priced in, or is there still genuine upside ahead?

- Does the rental yield on this specific property work at today's price, or am I banking entirely on capital growth that may take years to arrive

How ENAYBL Can Support Your Sydney Property Purchase

Whether you’re a first-time investor or building on an existing portfolio, Sydney’s combination of long-term capital reliability, constrained supply, and a persistently tight rental market presents a compelling case. At ENAYBL, we help property investors manage deposit requirements with our innovative deposit bond solution, keeping your capital free from exchange through to settlement. Contact us today to learn how we can support your Sydney property investment journey.

Frequently Asked Questions About Sydney Property Investment

Provided you buy the right product in the right location, it is a good property investment. Annual dwelling growth sits at 6.4% according to the CoreLogic Home Value Index, with five-year gains of 35% from an already high base. The market is underpinned by genuine population demand, a constrained land supply, and a rental market running well below balanced vacancy levels. It won’t match Brisbane’s 8% or Perth’s 13% annual growth right now, but it offers depth, liquidity, and long-term capital reliability that few other markets can. And is doing so from a median house price already above $2 million.

Compact, well-located apartments, particularly one-bedders in high-demand pockets, tend to offer the most workable yield-to-price ratios in Sydney’s current environment. With vacancy sitting at approximately 1.3% according to SQM Research, well-presented stock in desirable locations leases quickly and holds its tenant base. The critical filter is the building itself: owner-occupier-dominated complexes in established suburbs with genuine supply constraints will outperform investor-heavy new high-rise over any meaningful hold period.

Sydney’s annual growth of 6.4% sits behind Brisbane at around 8% and well behind Perth’s 13% but both of those markets are growing from a significantly lower base. Sydney is delivering that growth from a median house price above $2 million, with five-year gains of 35% already built in. Brisbane offers a more accessible entry point at a median of $1.17 million and a compelling near-term growth story. Sydney offers something different: long-term capital depth and permanence that comes from being Australia’s largest and most economically diverse city.

The main risk is what gets built around you. Zoning changes along transport corridors invite high-density development, and that new supply competes directly with your asset at every point, rental, resale, and refinance. CoreLogic data illustrates the outcome in Liverpool: houses up 14.3% annually, units up just 3.0% in the same suburb. Early buyers near newly announced stations can capture real upside. Buying into an established high-rise corridor after the announcement premium has already been priced in is a very different and often disappointing proposition.

A standard purchase requires a 10 to 20% cash deposit. On a $1.5 million Sydney property, that’s $150,000 to $300,000 sitting idle between exchange and settlement. For off-the-plan purchases where settlement sits 12 to 24 months out, that’s a long time to have capital doing nothing. ENAYBL’s deposit bond solutions provide a practical alternative, securing your position at exchange without locking away that cash. Contact the ENAYBL team to find out if a deposit bond is right for your next purchase.

The content of this blog reflects the personal views of the author and is for information purposes only. It does not constitute financial, investment or professional advice. Readers should conduct their own research and consult a qualified financial or property adviser before making any decisions to invest in property. The author and the blog are not responsible for any actions taken based on the content.